- GBP might be "gearing up for an important appreciation in the coming weeks"

- GBP recovers majority of March declines

- But a capitulation in global investor sentiment could trigger further falls

Image © Adobe Images

![]() - Spot GBP/EUR rate at time of writing: 1.1201

- Spot GBP/EUR rate at time of writing: 1.1201

- Bank transfer rates (indicative): 1.0900-1.0980

- FX specialist rates (indicative): 1.1040-1.1100 >> More information![]() - Spot GBP/USD rate at time of writing: 1.2337

- Spot GBP/USD rate at time of writing: 1.2337

- Bank transfer rates (indicative): 1.2000-1.2100

- FX specialist rates (indicative): 1.2200-1.2230 >> More information

The British Pound has advanced against the Euro and the majority of the world's largest currencies over the course of the past 24 hours but fell back against a resurgent U.S. Dollar amidst ongoing volatility due to the coronavirus economic crisis, however we have heard from a number of analysts who say the UK currency has potential to extend its recent recovery over coming weeks.

Sterling has in late March recovered some of the significant losses it suffered earlier in the month, a time that coincided with a significant global market financial meltdown owing to the global spread of the coronavirus crisis which appears to have triggered a sizeable outflow of foreign investor capital from the UK.

The Pound has fallen mainly against the safe-haven and 'funding' currencies of the Yen, Franc, Dollar and the Euro over the course of March, but the losses have been more than halved: the Pound-to-Euro exchange rate is down 2.3% but at one stage the scale of the losses in March stood at 9.0%, meanwhile the Pound-to-Dollar exchange rate is down 3.80% but had been as low as 11% from the point it opened its account for March.

Concerning the outlook, we hear from a number of analysts that this recovery can extend into April and even beyond.

"The GBP may be gearing up for an important appreciation in the coming weeks," says Shaun Osborne, Chief FX Strategist at Scotiabank.

Osborne says that the recovery in Sterling is however conditional on the UK announcing an extension to the timeline within which it seeks to secure a new trade deal with the EU. The call comes as EU and UK negotiators restart negotiations, this time via video link, but both teams are missing their respective chief negotiators who were both struck down by the coronavirus.

The UK and EU negotiators have until June to agree the foundation of a Canada-style trade agreement, with the view to completing negotiations by year-end. With the coronavirus crisis putting Brexit as a relatively minor consideration for EU and UK government's it is not hard to see what what was an already tight deadline has become even tighter.

Market anxieties concerning Brexit would lift should an extension be agreed, which could free up some headspace for further Sterling appreciation.

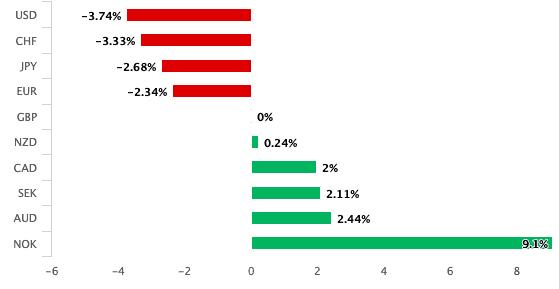

Above: GBP's performance against other G10 currencies over the course of the past month

Andrew Wishart, UK Economist at Capital Economics, is meanwhile looking at the other factors behind recent Sterling weakness when considering the currency's future and says there is more scope for bounce back in Sterling than was the case following the collapse witnessed in the wake of the Great Financial Crisis of 2008.

"The UK’s current account deficit is the main reason why the pound has fallen by more than other currencies against the U.S. Dollar over the past fortnight. The same was true in the Global Financial Crisis, and the Pound never really recovered. But the Pound was not overvalued going into this crisis, so there is more scope for it to bounce back this time."

The UK runs a current account deficit of close to 3% of GDP, which is one of the largest amongst developed economies, and is largely a result of the country importing more than it exports. Typically a currency would fall until such a time as imports and exports reached equilibrium. However, Sterling has over the years traded above this equilibrium point, propped up by significant capital inflows from global investors attracted to UK assets.

In times of market stress international investors tend to prove unwilling to finance the UK's current account deficit via investing in UK assets, in fact investment tends to flow out during such times, resulting in a situation that exerts increased downward pressure on Sterling.

"Occasional large falls in Sterling, which decrease the value of the UK’s foreign liabilities (denominated in sterling) and boost the value of its assets (some of which are denominated in foreign currency), is how the UK affords to run a near-permanent current account deficit," says Wishart.

Capital Economics research suggests the Pound was above its long-run trend and fair-value on a Purchasing Power Parity basis (of roughly 1.40 against the Dollar according to the IMF) heading into the Global Financial Crisis, it already looked undervalued on both counts this time around.

"The fall in Sterling in recent weeks has uncomfortable echoes of 2008, after which it never recovered. But the fact that the Pound looks somewhat undervalued give us reason to think that sterling will make up the lost ground this time around," says Wishart.

Capital Economics forecast the Pound-to-Dollar exchange rate to recover from 1.17 to about 1.25 by the end of the year, with the Pound-to-Euro exchange rate forecast to recover from 1.09 to about 1.14.

Above: GBP/EUR fell to levels not seen since the Great Financial Crisis and following the Brexit referendum this March.

Another reason for Sterling's vulnerability exposed by the coronavirus crisis lies with the country's outsized banking sector according to research from Nordea Markets.

"The UK has a large and systemically important banking sector which is particularly exposed in times of credit crunches and disturbances in the global funding system - containing Libor-OIS and basis swaps spreads via more USD liquidity is key," says Morten Lund, US & UK analyst at Nordea Markets.

![]()

Lund sees the Pound as being exposed to further declines against Sterling, and earlier this month told clients the currency was at risk of falling to parity against the Euro.

However, much depends on whether the stresses that impacted the global financial system, and by extension the UK's banking system, makes a return.

Analysts at Swiss investment bank UBS also recognise Sterling's exposure to the UK's financial sector as being a key weakness, however they say there is the prospect of a more sustained recovery in the currency going forward.

"We continue to see upside potential for sterling. Despite its relative liquidity, the pound was one of the G10 currencies most harshly punished by the dollar funding squeeze, possibly due to the UK’s large financial sector. As this issue seems to have been resolved, we expect sterling to regain its lost ground by mid-year. The Bank of England today decided to leave the measures it announced in previous weeks unchanged, which was interpreted positively by sterling investors," says Gaétan Peroux, Strategist at UBS.

The outlook for Sterling does however remain far from clear, particularly as the currency tends to struggle in times of global investor fear.

While the initial shock falls that characterised early March have given way to a recovery in global stock markets, there remains the possibility that we are seeing a bounce within a new bear trend.

The coronavirus crisis is a medical crisis at heart, and therefore requires a medical solution, something that is yet to transpire.

We therefore remain wary of further investor anxiety, particularly as the economic impact of the worldwide shutdowns translate into data and more businesses close doors permanently.

The world's economy is now widely forecast to slip into a deep recession that is being tipped by many economists to surpass the scale of the recession that followed the Great Financial Crisis of 2008, a scenario that tends to benefit the Dollar at the expense of the Euro, Pound and other major currencies.

"The unfolding global contraction is poised to supplant the GFC as the new benchmark for extreme economic disruption – the current collapse in economic activity is much deeper within individual economies and is enveloping a much broader range of economies concurrently than was the case in the 2008 crash," says Daniel P Hui, a Strategist with investment bank JP Morgan.